Getting ready for retirement is about more than having one’s finances in order, though that’s extremely important. It’s also about being mentally and emotionally prepared for a major life transition.

For those who are ready to retire in 2026, we wanted to take a look at their sentiment, readiness, and expectations for retirement. To do that, we surveyed 1,000 individuals ages 55+ in the United States who are planning to retire next year.

Respondents answered questions about their emotional and financial readiness, policy and legislative awareness, lifestyle expectations and concerns, and what a successful retirement means for them. They also shared their thoughts on delaying retirement.

Key Takeaways

- Retirement can look different to people based on their age and even generation, but being financially and emotionally prepared is key.

- Approximately 60% of respondents said they’re very confident that they’ll retire as planned in 2026, but the majority indicated they were either not very prepared financially or were only somewhat prepared.

- While many soon-to-be retirees feel excited, confident, or relieved to retire, others reported feeling anxious, uncertain, or overwhelmed.

- Concerns about Social Security, Medicare, and the rising cost of living are prevalent amongst those who are thinking about retiring in 2026.

- For many, the key to a successful retirement means being financially prepared, having a sense of purpose, and being able to spend time with loved ones.

Are You Ready to Retire? Retirement Timing

For many of our surveyed future retirees, 2026 is the planned retirement year, but there are factors that could affect if they actually retire this year or not. Some people choose when to retire based on age or health concerns, others on financial readiness.

Per our survey, people’s confidence in retiring in 2026 is across the board, largely due to financial reasons. Just over half, 60% of respondents, are very confident they will retire as planned. However, only 27% feel very financially prepared to retire, with 18% feeling not very or not prepared at all. A little over half (53%) feel somewhat prepared, falling squarely in the middle.

While retirees may have Social Security, pensions, and other income to support them, they also need sufficient savings. Out of our surveyed future retirees, only 46% felt that their retirement savings would support their desired lifestyle, so that may indicate a need to delay their retirement or ensure their supplemental Social Security and other income is enough for their current way of life.

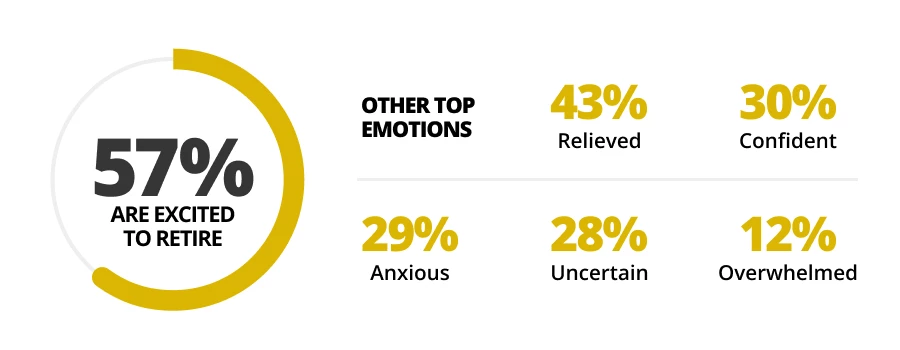

Emotional Retirement Readiness: 29% of Participants Feel Anxious When Thinking About Retirement

Financial stability is important, but deciding when to retire shouldn’t be based solely on money. After all, this is a significant life change. Being emotionally (and psychologically) prepared is key to a happy, productive retirement, whatever that might look like for the individual.

When asked how they feel about retiring next year, 57% of respondents said they’re excited. Other primary emotions were:

- Relieved: 43%

- Anxious: 29%

- Uncertain: 28%

- Confident: 30%

- Overwhelmed: 12%

While the majority are excited or relieved, there are some underlying concerns and uncertainties for our future retirees.

Emotional Preparedness

Like any major life event, retirement comes with its share of complex emotions. To determine emotional readiness, the National Active and Retired Federal Employees Association suggests asking the following:

- As you’re preparing for life after retirement, how do you prepare for the non-financial aspect?

- How do you define your purpose in retirement?

- What core values have helped guide you through life?

- How do you discover what you do best in planning life after retirement?

- What’s needed to create a vision for this next chapter in life?

- How do you research the resources needed to prepare for this vision?

- How do you rehearse for this next chapter while still working?

Ideally, the answers will help determine emotional preparedness for retirement.

Identity and Transition

Leaving the workforce behind can have a major impact on one’s physical and mental well-being. Some research suggests that retirement is largely beneficial for mental health, though its impact on general or physical health is less clear.

What does seem consistent is that working a satisfactory job, one that doesn’t interfere too much with personal life, gives people a sense of purpose. This is vital, considering maintaining a purpose in life is also associated with healthy aging. Our respondents do have concerns about losing their sense of self, with 40% citing concerns about loss of daily structure and loss of purpose.

This is a valid concern, and we’ve seen that with retirement, retirees lose the structure, role, and goals they had while working, which, for some, can lead to a loss of purpose and identity, as well as aimlessness. However, retirement can be an opportunity for renewed sense of self and purpose. With enough preparation, it can be a positive transition.

Hopes and Desired Experiences

Approximately 69% of our survey respondents said they’re looking forward to relaxation and less stress in retirement. But expectations don’t always match reality.

Our survey found that 52% dream of traveling more in their retirement, followed by seeing more family and friends (45%). With that being said, seniors make up only 37% of travelers as of 2023. This indicates that travel may not be an option for many retirees, for various reasons, including health and financial concerns.

While most people view retirement as their golden years, full of family, travel and reduced stress, that’s not always the case. Undue stress can lead to new or worsening health problems, especially in older adults. However, having a clear plan can make the transition from work to retirement less stressful, and more enjoyable. Planning ahead for retirement ensures you have a retirement plan built for your life, with contingencies for those unexpected events.

52% of Respondents Fear Outliving Their Retirement, Indicating a Lack of Financial Readiness

Financial readiness is also crucial, but what that looks like for one person might not be the same as for someone else. After all, everyone has their own goals and needs.

For example, someone who retires earlier than the average age of 62 might need more financial resources than someone who delays retiring by a handful of years. Someone else who intends to leave behind generational wealth will need a plan to sustain their net worth or assets.

Financial Preparedness

According to Empower, most retirees rely on four main income sources:

- Retirement savings vehicles like 401(k) accounts, annuities, and IRAs

- Social Security benefits

- Pension plans

- Continuing employment like part-time work or an encore career

Retirement plans, like IRAs and 401(k)s, have what’s called a “catchup” contribution. This exists to help those who started late saving for retirement. In 2026, the maximum contribution is:

- IRAs: $7,500 or $8,600 for those ages 50+

- 401(k)s: $24,500 or $32,500 for those ages 50+

However, 50% of our survey respondents said they haven’t taken advantage of catchup contributions in the past 5 years, which may further hinder their ability to retire comfortably.

Retirement Savings

According to Fidelity, people who want to maintain their current lifestyle should save around 10x their preretirement income by age 67. This means someone earning $100,000 should ideally have $1,000,000 in retirement savings.

Following this retirement savings rule can help, but it might not be enough on its own.

According to our survey, just over half (52%) of respondents fear outliving their savings, while another 36% are concerned about the high long-term care expenses that may hit. Only 21% of respondents are confident that their retirement savings will definitely support their desired lifestyle.

Financial Concerns

Approximately 74% of respondents flagged the rising cost of living as a top concern. Following this was rising healthcare costs (61%), Social Security changes (52%), and the fear of outliving savings (52%).

A Gallup study done a few years back found that 37% of adults 65+ were concerned about their ability to pay for healthcare services. Roughly a third of those ages 50+ skipped out on basic necessities like food to pay for medical expenses.

More recently, the National Council on Aging (NCOA) has linked higher mortality rates in older Americans with fewer financial resources. Those in the bottom 20% of wealth die an average of 9 years earlier than those in the top 10%.

As cost of living rises and life expectancy moves toward pre-pandemic levels (up to 78.4 years as of 2023), the fear of outliving one’s retirement savings is increasingly prevalent. For our 19% of respondents who are not very prepared or not prepared at all financially, this is especially concerning. We also found that 36% of our respondents said they would delay retirement due to personal reasons including family, health or lifestyle.

This emphasizes the importance of planning ahead financially for retirement and working with a professional who can help you be prepared for the worst case scenario, like a bad health diagnosis or family illness.

Policy and Legislative Awareness

There have been a lot of legislative changes recently that are affecting those planning on retirement within the next few years. Yet, according to our survey, 57% of respondents feel somewhat informed about legislative changes affecting retirement. However, 29% note they are not very informed or not informed at all about potential changes. This is especially concerning given how these changes can impact retirees and their future plans.

Heading into 2026, there are several key policy and legislative changes retirees should know about. A big one is the One Big Beautiful Bill Act (OBBBA).

The Committee for a Responsible Federal Budget estimates OBBBA will cause both Social Security and Medicare to become insolvent by 2032. Note that OBBBA doesn’t directly impact these programs, but it does reduce the revenue collected from income tax, which helps fund them.

Social Security insolvency could mean a 24% benefits reduction across the board (assuming no changes are made). Considering these retirement benefits are the primary source of income for 32% of retirees, this is a major concern.

Survey respondents cited changes to Social Security as most worrisome, with 37% of among soon-to-be retirees identifying that as the biggest legislative or regulatory change. Another 30% of respondents said Medicare changes are their biggest concern.

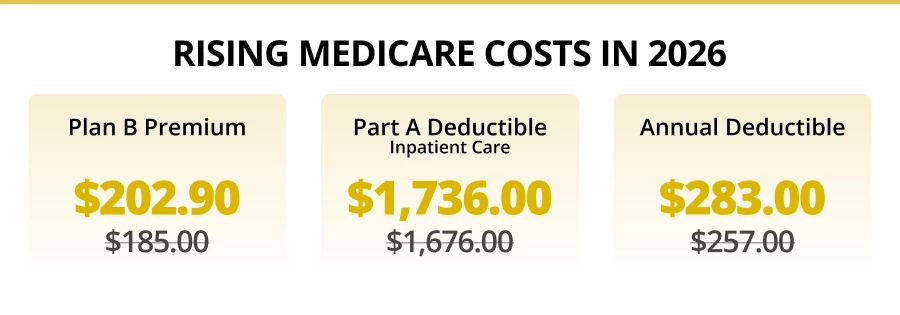

Medicare costs are expected to rise. The standard Medicare Part B premium increased from $185 to $202.90 in 2026. The annual deductible is rising from $257 to $283. The Part A deductible for inpatient care is going up from $1,676 to $1,736. With these increases, retirees will need to account for cost-of-living increases that may affect their retirement budgets.

Awareness is key as it can make all the difference between feeling ready to retire in 2026 and delaying. For those who are concerned about legislative changes, or even tax law and how it pertains to retirees, consulting a tax or retirement planning professional can help. A tax pro can also walk soon-to-be retirees through estate tax, required minimum distributions (RMDs), marginal tax rates, deductions, and more.

Lifestyle Expectations

Since retirement is both a major transition and unique opportunity, it’s not surprising that so many people would have expectations about what’s to come. Here’s what people look forward to most for their retirement years, as well as some concerns.

Positive Lifestyle Expectations

Research finds that retirement can provide a renewed sense of purpose. Many retirees expect to use their newfound freedom to experience the things on their “bucket lists.”

For some, the goal is to travel or pursue new hobbies or interests. For others, it’s to spend more time with family and friends. Whatever the case, staying active and engaged can lead to greater satisfaction in retirement.

Retirement’s also the time to focus on health and wellness, at least according to 44% of our respondents. This means socializing with loved ones, getting enough rest, eating nutritiously, and exercising regularly. It also means managing stress by spending time out in nature or with good people.

And while some people do go back to work after retiring, many do not. In fact, 78% of our survey respondents said they don’t anticipate going back to work for a non-financial reason.

Potential Lifestyle Concerns

Of course, retirement does come with a few potential concerns. Chief among them are loss of routine, social isolation, boredom, and changes to family dynamics. Finances are also a consideration for many soon-to-be retirees, particularly those on a fixed income.

One way to ease the financial burden (and reduce stress) is to downsize. Approximately 54% of survey respondents said they don’t plan on downsizing their home in retirement, but a quarter are unsure. Those who said they don’t plan on downsizing were then asked if they had concerns around the housing market that kept them from selling, but 82% responded that was not a factor. There are many reasons that retirees may want to stay in their homes, and as long as they’re prepared for any potential repairs or fixes that occur with homeownership, there’s no reason for the to immediately downsize as they step into this new chapter of their lives.

What Makes a Successful Retirement? According to Our Survey, Emotional and Physical Health

Success can look different to everyone when it comes to retirement. For our respondents, success is less about seeing specific destinations and more about their life as a whole. When asked what a successful retirement means to them, 62% of those surveyed responded with being emotionally and physically well. Another 57% said not having to worry about their finances, while 53% said spending more time with friends and family.

A successful retirement for one person might look completely different for someone else. That being said, these are the main factors contributing to it, and how retirees can prepare themselves for the changes ahead.

Financial Measures

Being financially prepared is vital to maintaining a preretirement lifestyle upon leaving the workforce. JP Morgan suggests planning for at least 35 years of living expenses — more if you retire early, expect to live a long time, or have other financial obligations ahead of you.

But it’s not just about having the money put away it’s how you put it away. We asked Stewart Willis, President of Asset Preservation Wealth & Tax, about the main factor people need to keep in mind when saving for retirement. “Tax deferral can be a time bomb in retirement. Consider the tax implications of decisions you make today and how that’ll affect you in the future. Most people put away money tax-deferred into retirement in the form of an IRA or 401k and they believe they’ll save money in retirement because their income is lower. What surprises them is not the tax they pay on that money when they withdraw it, but how that taxable income creates taxes and other penalties on things like Social Security and Medicare in the future. You may want to consider putting money away in post-tax assets like a Roth IRA.”

Also important is having predictable income. This could be from multiple sources, including retirement accounts and other investments. Those planning to claim Social Security might consider waiting until they’re 70 for the maximum benefit.

Last but not least, becoming debt-free can ease financial burdens. Interest can eat into retirement income (and savings), especially on high-interest or high-balance debts.

Emotional and Lifestyle Measures

Financial preparedness goes a long way for peace of mind, but it’s important to have a sense of purpose and emotional wellness going into retirement. This could mean picking up new hobbies, which require budgeting for, or taking on a part-time job to keep active and engaged.

Note that only 28% of survey takers said they’d continue to contribute via volunteering, mentoring, or part-time work upon retiring, which means they will need other opportunities to fill their previously full calendars. For some, this may look like joining a pickleball league, and for others it may be a relocation to restart their dating life in their golden years.

Legacy and Impact

Retirement is also a time for retirees to think about what they want their legacy to look like and how they can have further impact on others. This comes in many forms

For some, it could mean giving back to the community through volunteering or philanthropic donations. For others, it might mean mentoring younger individuals. Those intending to build generational wealth might need to start considering their estate (if they haven’t already), as well as set up plans for a wealth transfer.

What if Things Go Wrong? 37% of Respondents Cite Personal Reasons as Motivator Behind Delaying Retirement

Not every plan goes as intended. Some people may have to delay retirement beyond 2026 for reasons they didn’t expect — or sometimes even those they did.

When asked why they might delay retirement, 37% of survey respondents cited personal reasons due to health, family, or lifestyle. Economic uncertainty (36%) and healthcare cost concerns (33%) are the other main reasons to delay for those who are planning on retiring at some point this year.

The possibility of delaying retirement can lead to some complex emotions. Around 39% of those surveyed said the thought makes them feel disappointed, with 24% feeling conflicted. Another 15% reported feeling indifferent, 9% pressured, 8% hopeful, and 5% relieved.

All in all, 80% of respondents are very or somewhat confident about their transition to retirement. For those who are still unsure or are thinking about changing their plans, it’s not just about a lack of planning. Other variables, like legislative changes or unexpected health concerns, also play a role.

Planning Ahead for Your Retirement

Retirement planning takes a good deal of time and patience, but even then, plans can change. Being financially and emotionally prepared, as well as being aware of policy and legislative changes, can help ensure a successful retirement.

Whether you are retiring this year or several years from it, having the resources around Medicare guidance is important as you make this transition or solidify your plans. With 50% of our respondents wanting more guidance, it’s more important than ever to speak to a professional who can help with not only financial advising, but also healthcare and Medicare planning into retirement.

APWT is a great source of information on how to prepare for retirement. We can help you create a customized retirement plan based on your current financial situation. Schedule an appointment with one of our advisors to discuss your retirement plans and ensure you are ready for any unexpected changes.